We’ve made some improvements to our Betfair price importer that provides the prices for the backtesting.

Previously, we took a price snapshot once per second and wrote that to the DB for later retrieval in your strategies. 1-second intervals are obviously pretty granular (already resulting in about 10 million price snapshots per month of data!) and provide a good indicator of price trends and entry / exit points.

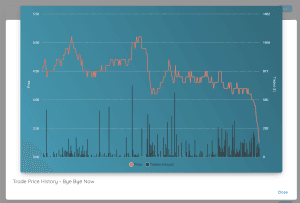

However when a race goes in-play, the prices obviously become very volatile and we’ve seen that the price can easily dip below or surge above the “snapshotted” price between snapshots, often for significant enough traded amounts that you would want to be aware of it in backtesting (where you’re basically always interested in whether the price touched a particular level).

To solve this problem without literally writing every tick to the database and needing a data-centre to rival OpenAI’s, we’re now analysing the ticks that make up each snapshot in memory and then storing the highest and lowest values as the snapshots.

The upshot of this is a more reliable indication of whether your entry or exit price was hit and therefore a closer correlation between your simulated backtesting results and your real life trading.

This will most benefit people who are exiting their trades in-running, or those doing lay the field type strategies.

Home of the best sports trading stats software